The international scientific and analytical, reviewed, printing and electronic journal of Paata Gugushvili Institute of Economics of Ivane Javakhishvili Tbilisi State University

Comparative Analysis of Development of Georgian Financial Markets

Summary

Existance of healthy financial markets is the important prerequisite for economice development of any country. It should be noted that the financial market consists of two very important segments, these are: Commercial banking sector and capital markets. These two segments are natural competitors. In Georgia commercial banking sector development is at a high level, but the capital market is still facing significant challenges, because, the stock market is monopolized by commercial banking sector.

Key words: financial markets, capital markets, commercial banking

Introduction

Over the past decade the state economic policy makes focus on creating strong foundations for shaping open and free market economy. This policy promulgates guaranteed protection of private property. [strategy 2020. 2013]. At the same time, valuable and efficient operation of market economy, based on private property principles, may be ensured through a constant supply of financial resources. This process is driven by financial markets. A financial market is a special mechanism for organizing a circulation of financial resources in economy [Toree, Schemukler, 2007]. It functions in the form of a debt capital market and securities market. Put it otherwise, this is a mechanism for capital distribution between creditors and borrowers, through mediators, based on capital demand and supply. In practice, it represents a combination of crediting organizations (finance-credit institutions), which direct money flows from owners to borrowers and conversely. Key mission of this market consists in transforming free money resources into loan capital.

By extension, the financial market with multi-component platform enables a businessman to favorably invest free money resources, on the one hand, and to draw the required capital with the best conditions, on the other hand, if he/she does not possess free money resources. Finally, this factor makes advantageous effect on economic development of the country.

The financial market can be structured in several dimensions: Equty and debt markets, primary and secondary markets, stock-exchange and OTC markets, money market, capital market and currency market [Bekaert, Harvey, 2000: 565-613].

Of the mentioned components, the developed countries have primary and secondary markets, stock-exchange and OTC markets. And primary and secondary markets are of crucial importance for normal functioning of modern market economy [Bakhtadze, 2011: 9].

In Georgia, the financial market segments may be associated with the bank loans market, on the one hand, and securities market, on the other hand, that comprises both corporate securities markets and government's T-bills market [Alen, Gale, 1997: 523-46]. Insurance industry and such segments as currency market, retirement funds (which are in incipience condition as part of government's mandatory pension reform), leasing companies, pawn shops and microfinance organizations hold a small ratio on Georgian financial market.

It should be noted that the latter entities segment holds so unimportant ratio on the financial market that they are not considered as competitors of the banking sector, on the one hand, and their role in financing the economy is very insignificant, on the other hand.

Banking sector and securities market industry

There are two key sources of financing economy and business in the developed countries: the banking sector and capital markets [Levine, Zervos, 1996: 329-39]. In Georgia, over the past decades, both sectors have passed certain phases of development, but we cannot say this period turned out successful for both segments. Today, Georgia's banking sector is a leader in the South Caucasus. Shares of Bank of Georgia and TBC Bank, Georgia's two leading commercial banks, are traded in the premium listing of London Stock Exchange (LSE). This is a genuinely great success that persuades investors of all levels in the world Georgia has steady and stable banking sector. We cannot say the same in relation to Georgia's securities market, which remains nonfunctional, in practice. It does not represent an efficient platform for investors and its financial indicators were not improved over the past 10 years.

Below we will introduce a comparative analysis of development of the mentioned two sectors, together with detailed analysis of each of them:

Banking Sector

After the 1990s collapse in Georgia, the banking sector emerges an only segment on Georgia's financial market that reached significant level of development due to various subjective and objective reasons and strengthened its market positions in the course of time.

Currently, sixteen commercial banks operate in Georgia, while in 1995 there were 102 commercial banks in the country. Modern technological progress, which has made positive effect on quality and promptness of Georgian banking services, as well as improved legislative regulations, have reduced the number of commercial banks. At the same time, the existing commercial banks have considerably increased and multiplied the number of service centers and branches.

In parallel, financial indicators of the banking sector have considerably improved. As a result, today, the ratio of assets of commercial banks in Georgia's finance sector accounts for 90% (evaluation of Georgian economy 2015 – Frankfurt School of Finance and Management). It should be also noted that despite 16 commercial banks, the market competition is weak, because 70% of the banking market is controlled by two major commercial banks. Therefore, it will not be exaggerated to say that the banking market is oligopolistic.

Despite the banking sector holds a dominating position in Georgian economy, it does not participate in economic growth because of multiple circumstances. In this respect, first of all, we should mention profitability index of the Georgian banking sector. Namely, if we compare net profit indicator of commercial banks with gross domestic product (GDP) of the country, that makes up 2.2%, and if we draw parallels with analogical indicators of such countries as Australia (2.9%), China (2.8%), Sweden (2.6%), Canada (2.3%), Netherlands (1.9%), Spain (1.8%), France (1.7%), Japan (1.4%), the USA (1.4%), Great Britain (0.9%) [WB, 2016]. Georgian banking sector, as compared to banking sectors of the developed countries, is one of the most profitable one, however, it is also worth noting that in the same countries, correlation of bank loans to GDP is very high, for example in China – 156%, Australia (142%), Great Britain (134%), Sweden (128%) and Georgia (53,1%). These figures show that in much more bigger and developed economies the banking sector's contribution to crediting economy is high, while net profits in relation to GDP are low. The situation is different in Georgia; loans' correlation to GDP is one of the lowest indicators – 53,1%, while net profits correlation to GDP is one of the highest ones in the world – 2,2%.

Analysis of structure of interest earnings of commercial banks also gives important information. In 2006-2016 incomes of commercial banks from legal entities was constantly declining. This indicator constituted 64% in total interest earnings in 2006, but the figure dropped to 40% in 2016. At the same time, revenues from consumer loans were constantly growing. This indicator was 36% in total interest earnings in 2006 and the figure rose to 60% in 2016. This dynamics shows that commercial banks make orientation on consumer loans mainly. Commercial banks prioritize consumer loans and they do not create wealth in the country. On the contrary, these categories of loans provoke an outflow of capital from the country (For example: buying imported products with installment payment schemes). At the same time, ratio of business loans declines year to year. This fact signifies that the banking sector, almost the only source of financial resources, makes unimportant contribution to the economic growth.

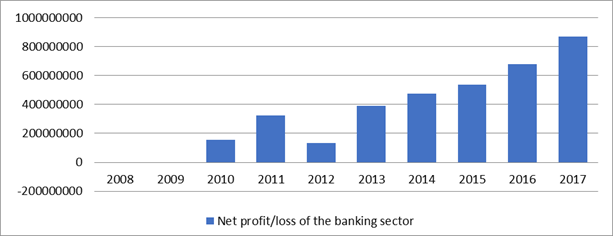

Chart 1

Net profit/loss of the banking sector

Source: NBG.GE. Remark: The 2008-2009 years for the banking sector were detrimental

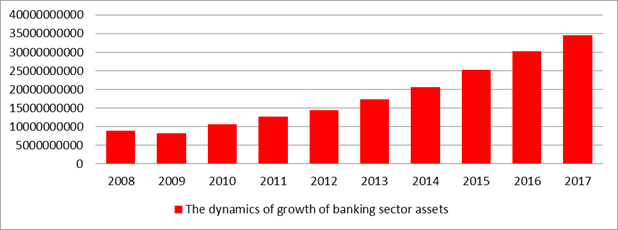

Naturally, when discussing the banking sector development issues, it is important to analyze its key financial indicators, including total assets and net profits. Over the years, both indicators have been growing constantly (excluding the 2008-2009 data after the 2008 August war). Namely: net assets of commercial banks from 2008 to 2017 rose by 289% and made up GEL 34.5 billion as of November 2017, while net profits rose by 456% in 2010-2017 period and hit a record figure – GEL 869 798 000 ( Chart N1; Chart N2).

Chart 2

The dynamics of growth of banking sector assets

Source: National Bank of Georgia

Deposits growth indicators are also important and it is one of the key factors for the banking sector development. The past 20 years have recorded considerable progress in this respect. In 1997 deposits at all commercial banks constituted GEL 91 million, 2% in GDP, while the figure hit 16 billion GEL in 2017, more than 50.2%. It should be also noted that population prefers to make savings in USD, compared to the national currency. As a result, deposits dollarization indicator is about 65%.

It should be also noted that the Government plays significant role in the banking sector development. For example, commercial banks mainly pay the profits tax, while other business pays excise tax, VAT and so on. Commercial banks' tax burden is at least twice lower, compared to other economic actors. Commercial banks constantly receive financial injections from the Government through a refinancing loan component of National Bank of Georgia (NBG), on the one hand, and only commercial banks have access to T-bills, on the other hand. Moreover, thanks to budget resources optimization reform over the past period, balances on the state budget treasury are deposited on accounts of commercial banks. We should also remember that Government of Georgia directed 850 million USD to the banking sector rehabilitation, out of 4.55 billion USD allocated by Brussels International Conference of Donors after the 2008 August war. In whole, the Georgian banking sector has a good development platform for many years thanks to active support from Government of Georgia.

Capital Market Industry

Capital market development in Georgia commenced in 1998, when, with the support of US leading experts, the country developed the securities regulatory law and, based on this law, the Authorities also started developing securities market key infrastructure: stock exchange, central depository, brokerage companies, registrars and the national securities commission of Georgia, an independent regulator of the securities market.

This law laid a foundation for securities market development in Georgia. This document comprises effective mechanisms for shaping a competitive environment, because there were threats that, at a certain point of development, the banking sector would try to engulf the competitor field (securities market) in its embryonic condition. Consequently, the law separated these two fields based on several important aspects, namely: commercial banks could not participate in the market (through only subsidiary brokerage companies); None of the stock exchange owners was entitled to hold a more than 10% stake in the exchange, while all commercial banks could not jointly hold more than 50% stake in the stock exchange; Supervision over the securities market and its participants was carried out by independent regulator –National securities commission of Georgia, which was a collegiate state regulatory management body and, besides supervision, its mission was to foster development of this industry.

Based on the law, as a result of separation of two competitor fields, the securities market in Georgia was being developed up to 2007-2008, basic financial indicators were growing, however, in the mentioned period an influential subjective factor emerged and the banking sector's lobby familiar to the previous Authorities realized that dominating character of commercial banks could be shaken. Therefore, they submitted a package of amendments to the regulator that resulted in suspension of the stock exchange development, in practice. According to these changes:

- Independent regulatory body was abolished and the securities market regulation was transmitted to National Bank of Georgia (NBG), the regulator of the banking sector, which is the competitor field to the securities market.

- Restrictions on the stock exchange ownership were abolished and commercial banks were enabled to fully subdue infrastructure of competitor field;

- Mandatory principle for making transactions on the stock exchange (for securities admitted for trading to the stock exchange) was canceled. As a result, 95% of securities transactions migrated to OTC market – to the opaque non-competitive, environment;

- Commercial banks were enabled to directly participate in securities market operations;

The mentioned amendments shook investor's confidence seriously. As a result, capitalization and turnover of the stock exchange shrank essentially. It may be said that the banking sector's plans for subduing the stock exchange and then artificial obstruction of its development was successfully fulfilled, since 5 brokerage companies of 6 ones operating on the Georgian Stock Exchange are subsidiaries of commercial banks. At least 40 brokerage companies operated.

Independent registrars were artificially ejected from the market, when the regulator National Bank of Georgia raised the minimum authorized capital amount to 250 000 GEL, only one independent, non-bank securities registrar remained on the market and at this stage, founders of even this only registrar have lawsuits against one of the leading commercial banks, since it was artificially pushed aside from the company founded by it.

As to the state regulation of the industry, as noted above, it is regulated by the National Bank of Georgia, which, according to established practice, avoids taking decisions, which could damage the banking sector's interests. In this case we have the clear conflict of interests.

Consequently, when government officials talk about their priority for the capital market development in Georgia and various mechanisms for its development, first of all, we should remember that the current legislation comprises no legal grounds for shaping competitive environment on the financial market. Therefore, all talks about significant development of the securities market industry are unrealistic without abolishing abovementioned amendments to the Law on Securities Market, since those were adopted under the pretext of the field deregulation (while having very specific pro-banking goals, as noted above).

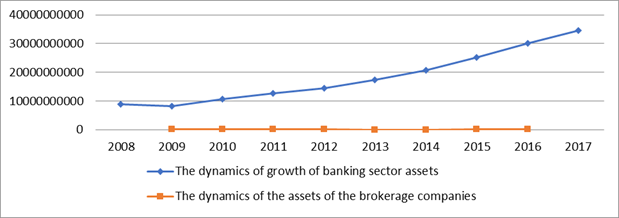

Chart 3

Dynamics of the growth of the brokerage companies and the banking sector assets

Source: based on nbg.ge; gse.ge – Authors calculation

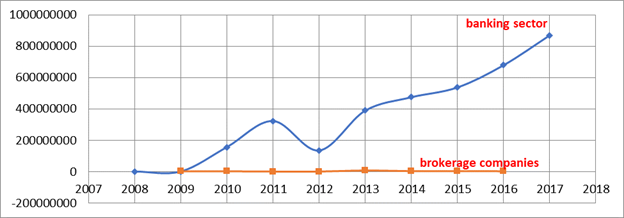

Chart N3 and Chart N4 presents a comparison of growth dynamics in assets and net profits of the banking sector and brokerage companies in 2008-2017 (a brokerage company in its nature is the same investment bank. Consequently, financial indicators of brokerage companies, as an influential institution of the stock market, are compared to financial indicators of commercial banks). Both cases clearly show that net profits of commercial banks and total assets are constantly growing, while in case of brokerage companies these indicators have not changed in practice after 2008 and even year on year downturn are recorded frequently.

Chart 4

Dynamics of net profit growth of banking sector and brokerage companies

Source: based on nbg.ge; gse.ge – Authors calculation

Conclusion

Financial markets in Georgia are not diversified, as the banking sector's ratio in the whole financial market exceeds 90%. This factor impedes economic development, because the comprehensive analysis shows that, despite dominating role of commercial banks, they does not participate in economic growth, in practice, and they makes focus on issuing consumer loans, but this instrument cannot produce economic wealth in the country, while, development of its key competitor, capital market, directs money resources straightly from an investor to the economy, via securities issued by companies or other bodies. Therefore, the capital market drives economic development more effectively compared to the banking sector.

Over the past decades, the Georgian banking sector was developed successfully with the active support of Government of Georgia; however, at the expense of absorption of other sectors of the financial market, in particular, the commercial banking sector has thoroughly monopolized the whole capital market infrastructure, thus blocking any attempts for development of its main competitor.

Consequently, to ensure normal competition on the financial market, it is necessary to improve the regulatory legislation, first of all, and clearly determine issues for separation of competitor fields.

References

- Allen F., Gale D. 1997. Financial Markets, Intermediaries, and Intertemporal Smoothing. Journal of Political Economy 105, pp. 523–46.

- Asian Development Bank's research. 2015. Financial health indicators, for stability of financial sector in Georgia. https://www.imf.org/en/Publications/CR/Issues/2016/12/31/Georgia-Financial-System-Stability-Assessment-42545

- Assessment of Georgian Finance Sector. 2015. Frankfurt Schools of Finances and Management.

- Bakhtadze L. Barbakadze Kh, Kandashvili T. 2012. Financial Institutions and Markets.

- Bekaert G., Harvey C. R. 2000. Foreign Speculators and Emerging Equity Markets. Journal of Finance 55, pp. 565–613.

- Capital Market Development Strategy (in Georgian). 2016. http://www.economy.ge/uploads/meniu_publikaciebi/ouer/kapitalis_bazris_ganvitarebis_strategia.pdf

- Demirguc-Kunt A. Feyen E. Levine R. 2011. The Evolving Importance of Banks and Securities Markets.

- Levine R., Zervos S. 1996. Stock Market Development and Long-Run Growth. World Bank Economic Review 10, pp. 323–39.

- The Georgian Capital Market Diagnostic Study and Recommendations. http://www.economy.ge/uploads/meniu_publikaciebi/ouer/CMWG_Diagnostic_Report_12_May_2015.pdf

- Torre A., Schmukler S. 2007. Emerging Capital Markets and Globalization. Stanford and Washington: Stanford University Press and The World Bank.